by Morgan Myrmo

"It is far better to be alone than in bad company." - George Washington

As investors have come to learn in the current bull market, there is a lot riding on interest rates. With monetary expansion uttering the new era of long-term economic growth, the simple threat of "turning off the pump" and letting the economy work with less Fed monetary influence has investors completely spooked.

The next meeting scheduled for the Federal Open Market Committee, or FOMC, is September 16-17, 2014. Most anticipate the winding down of the bond-buying program as anticipated in October 2014. Also, the consensus is that rates will stay at near-zero due to the most recent "Fedtalk."

The Traditional Fed Directive Demands Higher Rates Now

Traditionally speaking, the Fed actions have functioned to promote its dual mandate of full employment and price stability. With the great recession however, the Fed has become more of an "American monetary Godfather," using a strong, government-backed Keynesian approach.

To save the domestic economy from irreversible disaster, the Fed created the unprecedented monetary policies that continue today and are often referred to as "quantitative easing."

Also referred to as QE, or QE-Infinity to describe this continual, seemingly never-ending economic stimulus, quantitative easing has helped usher in a new era of stock returns as the current domestic bull market has clocked five consecutive years of positive annual returns.

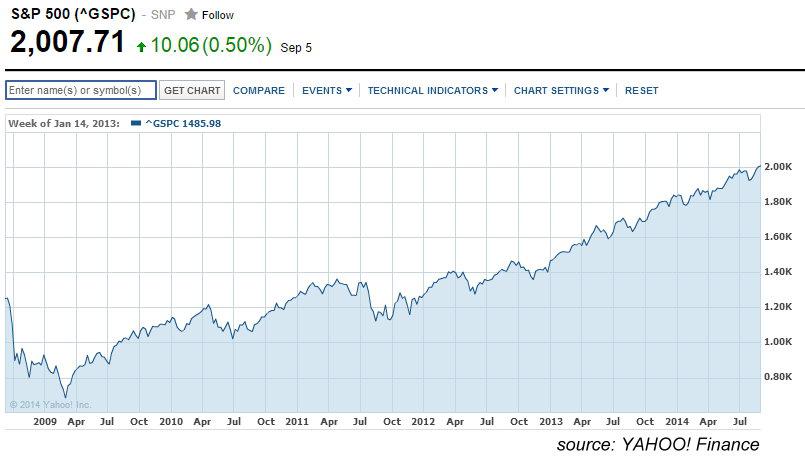

(click to enlarge)

2014 is on-trend to deliver the 6th-straight year of gains, with the S&P 500 Index up nearly 10% at 2007.71 (September 5, 2014).

(click to enlarge)

Just because the stock market has recovered and is setting all-time highs does not mean the Fed should raise rates and put an end to QE. There are more important indicators to consider, such as economic strength and of course employment and inflation statistics.

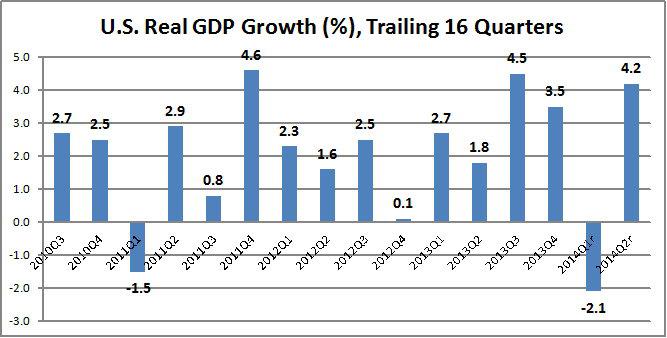

Economically speaking, the business cycle continues to improve, which clearly is lending a hand to stock market prices. According to the U.S. Bureau of Economic Analysis, the past four years have showcased continued economic growth, albeit with two quarters of economic contraction (most recently Q1 2014, -2.1%, adverse weather conditions blamed as major function of growth).

(click to enlarge)

While Real GDP is an important economic measure, it is more of a current indicator than a leading indicator. Looking at other measures will better forecast economic strength. The question that bestows us becomes not where the economy has been but where it is going and if the economy is forecasted to continually improve, then does the Fed need to continue with QE?

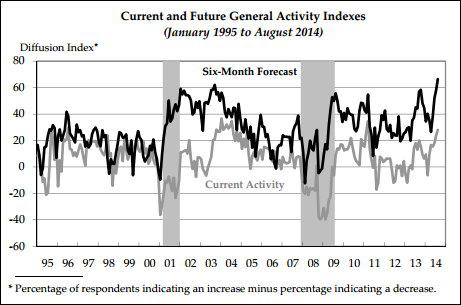

According to the Federal Reserve Bank of Philadelphia Manufacturing Business Outlook Survey, the Philly-Fed regional manufacturing sector continues to grow. According to the August 2014 survey newsletter:

"The survey's broad indicators of future activity increased, suggesting that firms remain optimistic about continued growth over the next six months."

Specifically notable is the overwhelmingly positive response that the economy will grow over the next six months (66.4%), while no respondents forecasted a decrease in business activity.

(click to enlarge)

Also to note, the diffusion index of current general activity reached the highest level since 2011, further suggestion that the regional economy is doing quite fine.

Philadelphia Federal Reserve Bank President Charles Plosser, in a speech on September 6, 2014, stated:

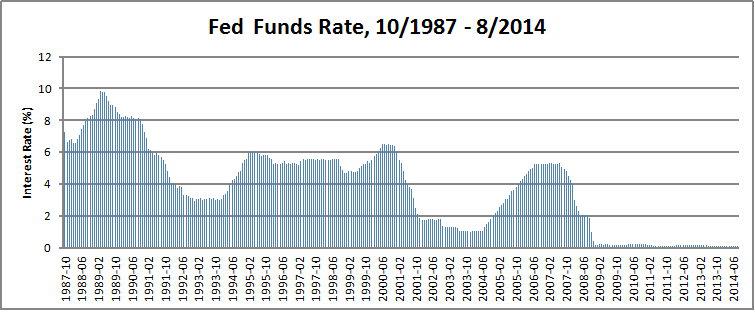

"The rate has been near zero for nearly six years now, and the Fed has augmented its aggressive policy actions through large-scale asset purchases, now tallying in the trillions, rather than in the billions of dollars. "

In reviewing the U.S. economy, Mr. Plosser continued:

"We are more than five years into a recovery that began in June 2009. While the pace has been sluggish and uneven, I believe the progress is undeniable. In fact, despite a winter cold spell in the first quarter, I remain mostly positive about the prospects ahead."

Regarding the lower-than-expected gains in August payrolls, Plosser cited the YOY trend is upward and showcases continued employment strength.

" I prefer to look at longer-term trends rather than monthly numbers that are still subject to revision. Year-to-date monthly average job growth has amounted to 215,000 jobs this year, compared with a monthly average of 194,000 jobs added last year.

Despite the slowdown in August, job creation has improved markedly this year. The economy has created 1.7 million jobs since the start of the year, nearly 10 percent more than the same period in 2013, 20 percent more than in 2012, and 30 percent more than in 2011.

The unemployment rate was 6.1 percent in August, down more than a full percentage point from a year ago. This means the unemployment rate continues to fall faster than many policymakers had been forecasting."

Plosser continued with information regarding inflation, which is trending upward and has recently been forecasted to reach 2% by 2015.

The Philadelphia Fed's most recent Survey of Professional Forecasters also increased its average estimate of headline PCE inflation to 1.8 percent in 2014, up from 1.6 percent in the last survey. The survey also increased the estimate of PCE inflation to 2.0 percent in 2015, up 0.1 percentage point from the previous estimate.

All of these figures suggest that inflation appears to be gradually moving closer to our target of 2 percent and doing so more quickly than anticipated in December 2013."

So when it comes to the dual mandate of the Federal Open Market Committee, of which Plosser is a member of for the remainder of 2014, it seems that a quicker-than-anticipated ending of QE should be required.

To back up the Philadelphia Business Outlook Survey, the August 2014 ISM Report on Business, released September 2, 2014 (four days before Plosser's speech), stated the following:

"The August PMI registered 59 percent, an increase of 1.9 percentage points from July's reading of 57.1 percent, indicating continued expansion in manufacturing. This month's PMI reflects the highest reading since March 2011 when the index registered 59.1 percent."

Clearly the trend is positive, with manufacturing expanding faster than average on the year.

Both FOMC member Plosser and the ISM are showcasing strong manufacturing data, which is backed up by continual growth in real GDP and strengthening employment data. So what is the Fed to do?

The Fed Should Raise Rates Now

To recap what most investors already understand, the dual-mandate of the Fed is to help the economy achieve full employment and ensure price stability. Currently domestic unemployment is at 6.1% and the economy has been adding on average 215k jobs per month this year, a 10.8% increase versus 194k monthly jobs in 2013.

Regarding PCE inflation, the inflation measurement the FOMC regards, Plosser revealed last Friday in his speech that inflation expectations of 2% for 2015 and inflation "appears to be gradually moving closer to our target of 2 percent and doing so more quickly than anticipated in December 2013.

While there is no agreed-upon definition of full employment and Plosser does acknowledge somewhat of a frustrated workforce, 6.1% unemployment is a giant step for the economic rebound. In his recent speech, Plosser states:

"Many Americans remain frustrated and disappointed in their jobs and job prospects. For example, there remains a large contingent of those working part time for reasons economists don't fully understand. Nonetheless, we have to acknowledge that significant progress has been made."

In other words, the Fed has succeeded in bringing the economy up to speed in terms of employment. With PCE inflation expectations of 2% coming sooner than anticipated just nine months ago and employment at or near full, it appears that the Fed has succeeded and that now is the time to raise rates.

Why Now, Why Not Later?

While the Fed has increased the money supply during QE, which is finally set to end in October 2014, the economy has been able to achieve relative price stability and job growth.

With a huge balance sheet now, the Fed needs to look at an exit strategy to tame inflation. A slow rise in interest rates, whilst keeping to an era of low-interest rates, would ensure dollar strength and continued positive real GDP growth.

Economic uncertainty, which would be created by rapid interest rate hikes, would spook business and investors would retreat quickly. Leave rates too low for too long and high interest rates would be required to tame inflation, which would come at the price of lower real estate prices, reduced consumer spending, lower GDP growth and increased stock market volatility.

What Will The Fed Do?

I believe the FOMC will raise rates sooner than the investment banks and markets anticipate. Goldman Sachs (NYSE:GS) believes that the rates will start to rise in October 2015, however with a strong economy, 6.1% unemployment and a sooner-than-later 2% PCE expectation blooming, the FOMC will have to act faster than expected.

What markets need to realize is that it's not the first rate hike that impedes economic growth, it's the continued rate hikes that the market does not expect that would threaten uninterrupted annual real GDP growth.

The Fed will have to change "verbiage" to reflect this. For the markets to stay in sync with the Fed, Janet Yellen should showcase an anticipated March 2015 hike to 0.25%, followed by the likelihood of another hike to 0.5% in October 2015.

(click to enlarge)

The current fiasco in Europe (on September 6, 2014 the ECB cut rates to near-zero and announced new QE, bond-buying measures) will only increase global demand for the dollar and dollar-denominated debt and equities into 2015. With slightly higher rates, additional collar-debt demand could in fact keep the 10-year treasuries at ~2.5% to ~2.75%.

In addition to stable, low-priced debt, the slightly higher interest rates will help stifle inflation, improve bank profitability, keep housing and commercial real estate prices stable and support continued positive real GDP growth.

No comments:

Post a Comment