by The Economist

Throughout the rich world, wages are stuck

CENTRAL bankers once used to inveigh against wage inflation. Guarding against a return to the ruinous price-wage spirals of the 1970s was a constant preoccupation. Since the financial crisis, however, they have started to fret about the opposite concern: stagnant wages and the growing risk of deflation.

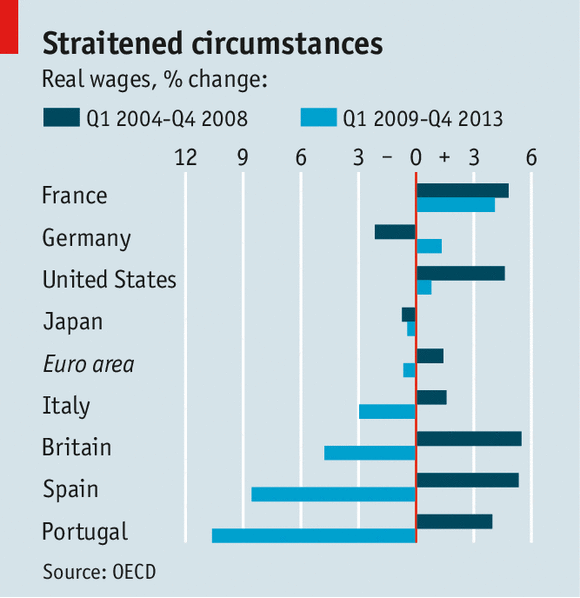

| There has been a squeeze on pay in the rich world for several years now. Between 2010 and 2013 real (inflation-adjusted) wages were flat across the OECD, according to its annual “Employment Outlook”, published on September 3rd. Real wages have barely grown at all in America over that period and have fallen in the euro area and Japan (see chart). Declines have been particularly sharp in the troubled peripheral economies of the euro zone, such as Portugal and Spain, but real wages have also tumbled in Britain. In most advanced countries—though not in Britain or Italy—labour productivity is picking up again. Moreover, the downward pressure on wages from high unemployment is easing in some countries, including America and Britain (in the euro area, alas, the jobless rate is still 11.5%). Yet even though unemployment in America has dropped from a peak of 10% in late 2009 to 6.2%, growth in even nominal wages (ie, not adjusted for inflation) is tame. In the private sector, they had been rising by around 3.5% a year before the crisis, but are currently increasing by less than 2% a year. In Britain, where unemployment has fallen from a peak of 8.4% to 6.4%, nominal pay is growing by 0.6% a year, far below the pre-crisis average of 4%. |  |

Divergent trends in the supply of labour help to explain why the pay squeeze has been more intense in Britain than in America. The British labour participation rate—the proportion of adults who are either in work or looking for jobs—has returned to its previous peak of almost 64% and looks set to rise further. By contrast, America’s participation rate has declined by three percentage points since the financial crisis and is now bumping along at around 63%.

Working out to what extent the low participation rate is structural, meaning that it will persist, rather than cyclical, caused by a weaker-than-usual recovery, will be crucial in determining when the Federal Reserve raises interest rates. The Fed has seen quiescent nominal wages as evidence the labour market has more slack than falling unemployment suggests. But Janet Yellen, its chairman, recently said that the weakness in wages might be deceptive. New research by the San Francisco Fed suggests that many employers froze pay during the recession because workers resist cuts in nominal pay more fiercely than the erosion of their purchasing power by inflation. Employers, unable to reduce wages when times were bad, have not been raising them now that times are better. But once this “pent-up wage deflation” has run its course, pay growth might take off.

Such a rebound may occur outside America, too, since there has been a widespread—although by no means universal—reluctance to cut nominal wages across the OECD, according to this week’s report. Between 2007 and 2010 there was a big jump in the share of workers whose wages remained flat in nominal terms. In Spain, for instance, the proportion of full-time workers having to accept pay freezes rose from 3% in 2008 to 22% in 2012.

Weak Japanese wages are worrying Haruhiko Kuroda, who as governor of the Bank of Japan is in charge of his country’s latest attempt to vanquish deflation. A new programme of quantitative easing—creating money to buy bonds—has been more successful than previous, half-hearted attempts to get prices rising again, but wages have remained sluggish. Although cash earnings jumped by 2.6% in the year to July this largely reflected bigger bonuses; regular pay rose by only 0.7%, well below the newly revived level of inflation. Mr Kuroda recently said that a “visible hand” was needed to co-ordinate higher wages.

Such a solution smacks of desperation but it might work in Japan, which retains its currency. It would not make sense for the euro area, the other big economy where deflation remains a risk. Prices rose by just 0.3% in the year to August, but in a currency club it is vital to allow wages to rise and fall freely to provide the internal equivalent of fluctuating exchange rates.

If wages in Germany rise, the downward adjustment in less competitive economies in the euro zone need not be so severe. That is why Jens Weidmann, the head of Germany’s central bank, has been calling for higher pay—a daring step in a country of inflation hawks. The European Central Bank, which cut interest rates this week, could also act more boldly to raise inflation towards its target of almost 2%. That would allow the euro zone’s invalids to regain competitiveness through wage freezes rather than outright cuts.

Wages, of course, are not just important to central bankers. Weak pay saps revenue from income tax and social-security contributions, making it harder for governments to mend public finances. The lack of growth in real wages hurts household finances, too, keeping consumers tight-fisted. A healthy and sustained recovery in the rich world will remain elusive until the pay squeeze ends.

No comments:

Post a Comment