Summary

- The first 2 CDS ETFs have just hit the U.S. market, making it easier for individual investors to gain direct exposure to credit risk.

- With credit spreads near historic lows, it is inexpensive to bet on declining credit quality using WYDE, an ETF that is short high yield credit default swaps.

- Credit default swaps have the potential to deliver strong positive returns when other asset classes are plummeting.

- WYDE has significant negative correlation with equities, so owning a position in the ETF helps reduce portfolio volatility.

Proshares just introduced 2 new ETFs tied to credit default swaps (CDS), for the first time giving the average investor the ability to directly take a position in credit risk. These 2 ETFs give investors exposure to the credit of U.S. based, high yield issuers, with the CDS North American HY Credit ETF (BATS:TYTE) taking a long position (betting on improving credit quality), and the CDS Short North American HY Credit ETF (BATS:WYDE) taking a short position (betting against credit quality). I believe this represents an extremely attractive time to invest in WYDE, due to strong return potential and significant portfolio diversification benefits.

Credit Default Swaps in a Nutshell

When an investor buys a bond, they are indirectly investing in a number of components making up the bond, including its risk free return, its associated credit risk, its sensitivity to interest rate movements, and prepayment (for callable bonds), extension and other risks.

Credit default swaps allow an investor to isolate the credit risk in a bond or group of bonds. An investor who is short a CDS can remove credit risk from their bond investment, allowing them to focus on the other risks inherent in fixed income investing. An investor could also go long a CDS instead of buying a bond to isolate the return from credit risk without worrying about the other risks involved in owning a bond.

Each CDS is a contract between 2 parties which transfers credit risk from one party to the other. The person that is short the CDS is essentially buying insurance; they pay the party that is long the CDS a fixed payment, and in exchange the long will cover any losses on their investment. High yield CDS have a standard payment of 5% a year, with the price of a CDS adjusting to effectively increase or decrease this spread to an appropriate market rate. At the time WYDE started trading its weighted average CDS spread was 3.42%, with this spread tightening slightly since it was issued leading to a moderate price decline.

WYDE and TYTE cover the credit of the North American high yield market through the use of the Markit CDX NA High Yield index. The CDX NA High Yield index is made up of the 100 most liquid individual company credit default swaps within North America which have below investment grade credit ratings, with each of these companies equal weighted at 1% of the index. The index is rebalanced twice a year, taking out companies which no longer qualify to be in the index and removing companies that have defaulted.

For each defaulted company a determination is made as to its recovery rate (which is the amount bondholders will receive from the defaulted company); based on this recovery rate, the CDS buyer receives money to compensate them for the amount of money they lost, making their investment in the bond whole. Below is an example given by Markit:

Assuming a recovery of 70 cents on the dollar, all protection buyers are compensated 30 cents in the dollar on the defaulted name. For LCDX contract holders, where each entity has a 1% weighting in the index, they are compensated 1% * 0.3 multiplied by the notional of the LCDX trade. For a $10m trade, this is $30,000.

Investing in either TYTE or WYDE lets an investor take direct exposure in the loss rate of a portfolio of high yield bonds. Whether used for hedging, speculating on credit changes or for portfolio management purposes, these new ETFs open up a new range of opportunities to individual investors which were previously only available to high net worth individuals and institutional investors.

The Opportunity

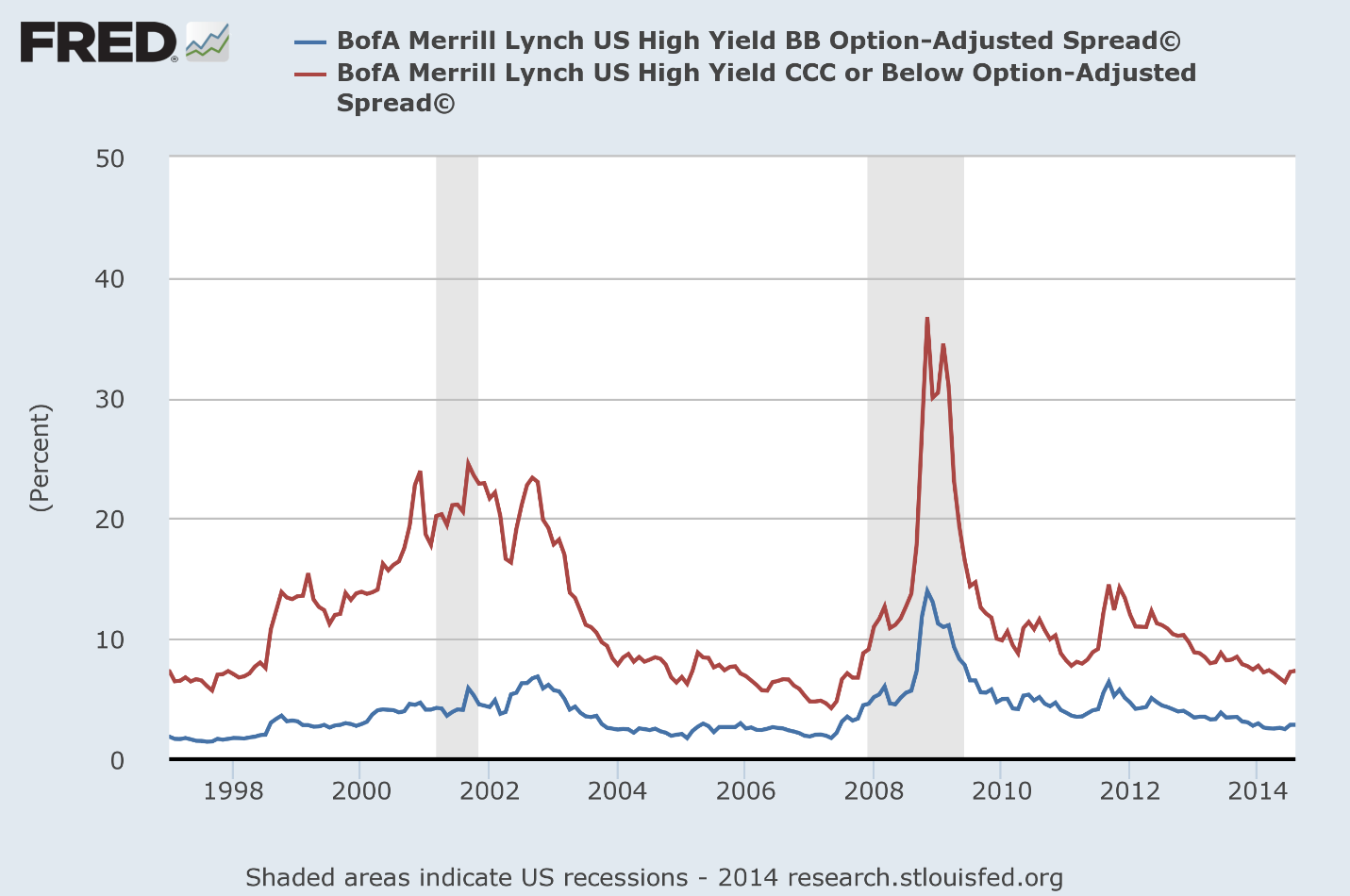

Right now, credit spreads are hovering near all-time lows (shown below), meaning now may be the best time to enter into a short CDS position. With credit spreads this low, buying into a short CDS position can be done at a rock-bottom low cost with a far greater opportunity for price appreciation.

(click to enlarge)

(Image borrowed from an article by Robert Singarella Jr.; I'd encourage readers to view his article for a contrary perspective.)

With the NA CDX High Yield index tracking a portfolio consisting of companies rated BB and below, its spread will fall somewhere between the 2 lines in the chart above, as it holds swaps covering the credit of companies with ratings between those lines. When the credit spread increases it causes an increase in the price of WYDE, the short CDS party, and a decrease in TYTE, the party long the CDS. Correspondingly, a decrease in this spread would lead to a decrease in price for WYDE and an increase in price for TYTE.

CDS pricing has a high correlation with credit spreads as an investor can buy an equal weighting of each of the 100 bonds in the index, enter into a CDS to protect against their losses and earn a risk free rate of return. If the CDS were trading at a lower spread than the same portfolio of bonds, an investor could buy the portfolio of bonds with a high spread (say 5%), enter a short CDS at a lower spread (say 4%) and earn a risk free profit (of 1%).

Because of the large amount of liquidity in the CDS market, overall pricing should reflect this credit spread in order to prevent investors from engaging in this arbitrage opportunity, with the high liquidity of individual company CDS's also helping to enforce this relationship. Although the correlation between credit spreads and CDS pricing will not be perfect (due to the 5 year contract length, the 100 company sample, and the price of the contract corresponding to future credit losses, not the spread), this does help decipher the underlying fundamentals behind CDS pricing. This also helps show how the current historic low in CDS pricing represents a longer-term opportunity, as defaults and credit spreads have almost nowhere to go but up.

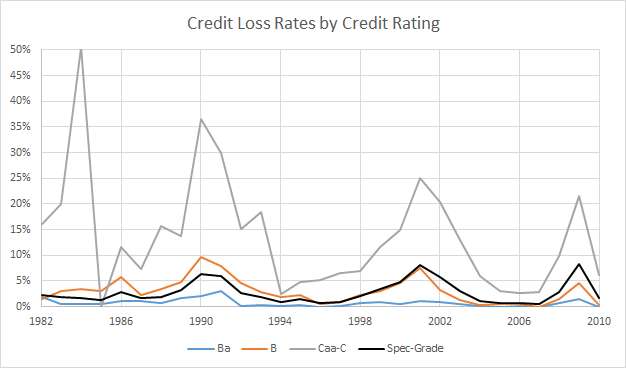

A large part of the return to an investor in WYDE or TYTE will be from changes in the price of the CDS, especially over shorter time frames. Over the lifetime of a CDS contract however, profits are determined by the CDS' cash flows, with the loss rates on the underlying constituents paid by the long party less the fixed coupon paid by the short party determining the overall return to each investor. Looking at historic loss rates (shown below) helps to estimate the cash flows and fundamental value underlying the CDS. Overall, loss rates have a high correlation with credit spreads, but with smaller absolute changes, as credit spreads are forward looking estimates of default rates (and therefore prone to significant judgment), which are often made with limited information during high stress, high risk environments.

(Source: Moody's)

According to Moody's, between 1982 and 2010 the average speculative grade credit loss rate was 2.78%, meaning that over the long run investors that have been long credit default swaps (those taking on the credit risk) have earned a profit. This makes sense as they are essentially selling insurance and expect to profit over the long term from taking on added risk. At current credit spreads of less than 3.5%, the premium for taking on credit risk is minimal, with this "insurance" costing only 50 basis points above the average loss rate experienced over the last 3 decades.

The reason for this low spread is that defaults have been low in recent years, with current defaults near historic lows of 1.8%, helping to fuel this incredible decline in credit spreads, and creating this opportunity in WYDE. Although defaults are not likely to spike in the near term, the current spread provides an impressive entry point for investors looking for an eventual spike in defaults.

Credit Quality Trends in the U.S. Market

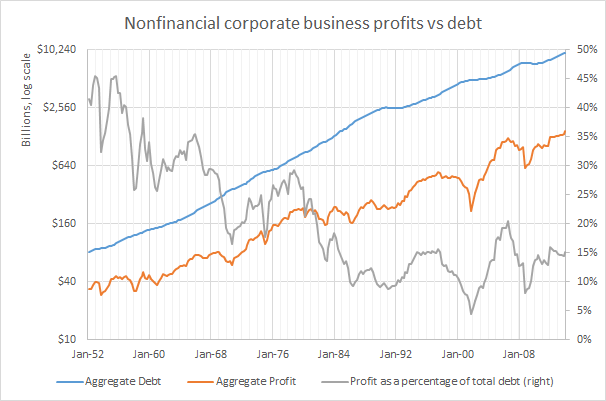

Another factor which makes investing in WYDE an attractive proposition is the overall decline of corporate credit quality over the last few decades. The graph below shows aggregate profits and aggregate debt levels of U.S. based non-financial corporations on the left axis, with their total profits expressed as a percentage of debt on the right axis.

(Source: Federal Reserve data, Z1)

Overall debt has risen at a much faster rate than profits, with this trend starting in the late 60's and early 70's but accelerating during the debt-fueled leveraged buyout craze of the 80's. This trend has continued recently as well, with profits rising only 16.7% since the last market peak of Q3 2006 with debt increasing by 57.4% over this timeframe. As of now, it would take 6.6 years of non-financial corporate profits to repay cumulative debt, with this figure seeing levels as low as 3 years as recent as the 60's. Since this is an aggregate figure, many corporations are in far worse shape than this average, especially companies in the high yield bracket.

A higher level of debt relative to profits means that when the average company's debt comes due they are less likely to be able to fund the repayment of principal through internally generated funds. This can have the effect of creating situations where a company is forced to enter the capital markets during inopportune times, either at a time when the company is experiencing a slowdown in sales or during recessionary periods where it is more difficult to draw in funds. At higher levels of debt a company has less room for error, and is more prone to default if business or financial market conditions worsen.

The effect of swings in profits on debt coverage also helps to highlight why equity markets and credit markets (especially high yield) are so closely correlated.

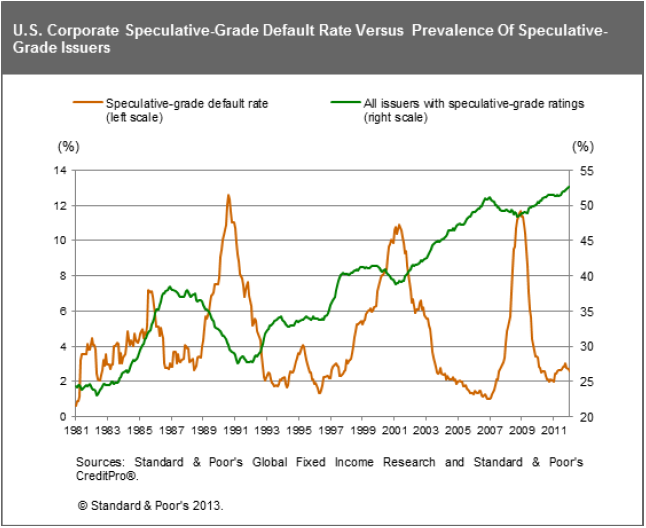

Despite the large amount of negative things that have been said about credit rating agencies, they have factored in this massive increase in corporate debt in their ratings, with the proportion of companies with below investment grade credit ratings increasing dramatically over the last 3 decades (as shown below).

(click to enlarge)

(Source: S&P)

Despite the current low levels of defaults, this continued decline in credit quality should eventually lead to another spike of defaults over time.

Catalysts

Investors in WYDE also benefit from a number of medium-term catalysts.

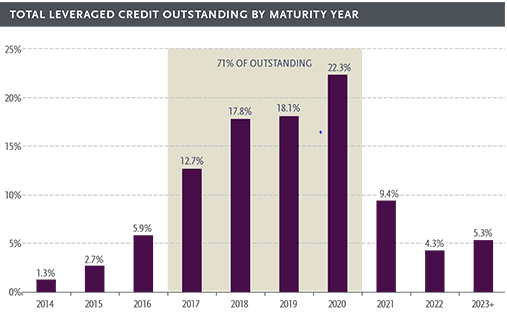

First amongst these catalysts is the upcoming maturity of a large amount of high yield debt (shown below, with these figures from 12/31/2013). The maturity of debt creates a reevaluation of business prospects, resetting both the interest rate and risk spread to the new market levels. If business or competitive conditions have worsened for a company, it creates a situation where the market may demand a significantly higher coupon in order to refinance its debt, adding to the struggling company's burdens. During periods where a greater number of companies are forced to refinance their debt, defaults are inclined to reach higher levels, especially if it coincides with a period of general market weakness.

(Source: Guggenheim)

Adding to this refinancing issue will be the eventual rise in interest rates over the next few years. High yield companies have benefitted from historically low financing costs due to both record low risk-free interest rates and record low credit spreads. With both of these values poised to rise over the next few years this will put added pressure on high yield companies, further increasing default pressure.

Conclusion

This combination of above average default potential, historically low cost and significant room for price appreciation gives WYDE a good chance to deliver positive returns going forward. Coupled with significant negative correlation with equities, it is a good candidate for inclusion in a conservatively minded portfolio looking to hedge away credit risk or diminish equity related risk.

No comments:

Post a Comment