Stock markets in emerging markets (EMs) have gotten off to a rough start this year after a challenging 2013. Valuations have fallen and volatility remains high. So should investors add exposure to emerging markets—or is it better to steer clear?

In our view, it’s probably too early for a large tactical shift towards emerging markets. But we do think the time is right for investors who are underweight EMs—or who lack exposure altogether—to start rebalancing towards their strategic targets in developing-world stocks. While short-term caution is appropriate, we think EM stocks continue to provide a good long-term opportunity—especially for active managers.

New and Old Problems

EM stocks’ underperformance started with the Fed’s tapering talk, but now the spotlight is on endogenous problems. These include some that have traditionally plagued emerging markets, notably the troubles in the “fragile five”—Brazil, India, Indonesia, South Africa and Turkey—which depend on foreign investment flows to fund domestic deficits and are more at risk from currency depreciation. And as Russian stocks plunged this week in response to the Ukraine crisis, investors received a stark reminder that political instability is a fact of life in key emerging markets.

Newer threats are also worrying investors. These include China’s slowdown and the need for structural reforms in several large EMs, including the BRICs (Brazil, Russia, India and China), which could suppress growth. Fears of a credit crunch are also rife after a rapid credit expansion in many EMs; several banking systems—and large EM companies with heavy benchmark weights—could be vulnerable.

Reasons for Resilience

However, we think these concerns have also obscured some key reasons why most developing countries are likely to be more resilient than in past crises:

- External independence—with the exception of the fragile five, most larger developing countries today have strong public finances and large foreign currency reserves

- Low inflation—monetary policy should remain accommodative, except in countries with external deficits that are raising interest rates to defend their currencies

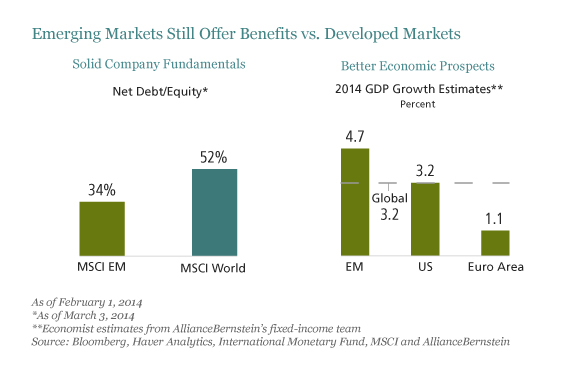

- Company resilience—balance sheets of companies are typically strong and there is often more scope for margin improvement than in developed-market counterparts (Display, left chart)

We also think worries about China are overdone. Although the days of double-digit growth are over, we expect growth to stabilize at about 7.5% a year. This still would represent a huge engine for demand from the world’s most populous country.

Why Maintain Exposure?

We believe that there’s still a compelling longer-term case for significant EM equity exposure within a diversified portfolio. Emerging-market equities can provide better long-term earnings growth from access to the rapid economic growth that is typically fueled by stronger productivity growth. In some countries, working age populations are growing much faster than in developed markets. And valuations today are once again significantly lower than in developed markets.

Diversification is another benefit. Although correlations between emerging and developed markets have increased in recent years, last year reminded us that they often still behave very differently. And within emerging markets, investors can diversify further by including smaller markets; stocks in the United Arab Emirates, Qatar and Vietnam markets have done very well this year.

Good Conditions for Active Management

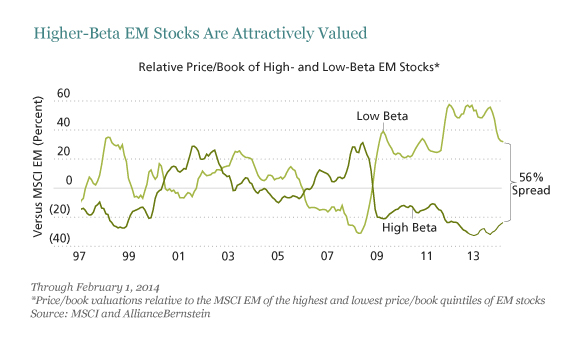

In today’s volatile conditions, we think stock picking is the best way to go. Spreads are unusually wide between higher-beta, more cyclically exposed stocks, and “safer” low-beta stocks (Display). While some of these stocks, for example in basic commodity sectors, may deserve low valuations, our research suggests that others look more promising, such as Indian cyclicals. There are also many high quality companies with solid fundamentals and high return on equity to be found.

We’re wary of taking a passive approach and just buying an index. Since last year’s sell-off was not uniform, it has accentuated some already large pricing discrepancies that are creating rich pickings for bottom-up stock pickers. And the stocks that win in the years to come are likely to be very different from the winners in the last five, as the sources of growth in emerging markets shift. Meanwhile, macro risks vary widely by country and are not always fully reflected in pricing differentials; so, in our view, it’s especially important to discriminate in country exposure within a portfolio.

Emerging markets have always been volatile—but that’s one of the reasons why they have also delivered higher returns than developed markets over time. We think it’s no different today. In our view, investors with a long-term horizon should maintain their allocation to emerging-market stocks.

No comments:

Post a Comment